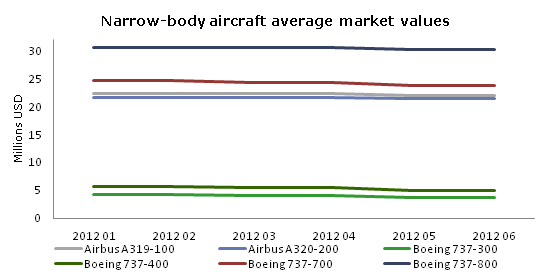

Economic uncertainty continues to force down prices for narrow-body aircraft

The first half of 2012 was quite unsurprising in the aircraft market as the prices continued falling. Although all aircraft cost considerably less than before, as expected, the biggest price drop could be spotted on the price-tags of the older generation aircraft. The cost of the Boeing family – B737-300 and B737-400 models dropped by 13% in comparison with the 2011 end/ 2012 beginning rates.

Extensive demand

‘Boeing 737 aircraft remains to be one of the most popular aircraft types in the world. During the first half of 2012 over 250 B737s were sold, leased or delivered. Moreover, additional aircraft are being re-delivered to the global market, since the recently bankrupted carriers, particularly the larger ones, are returning or selling out their fleets. Such ample offer of aircraft on the market is one of the main (and natural) factors which continue to push the prices down,’ commented the Deputy CEO of AviaAM Gediminas Siaudvytis.

Table 1. Narrow-body aircraft average market values, June 2012 vs January 2012

At the same time, due to financial difficulties in 2012 alone three large European carriers – Malev, Spanair and Olt Express Poland – were forced to file for bankruptcy. Their fleets, consisting mainly of aircraft “classics” like Boeing 737 and Airbus A320, as well as the fleets of other air companies which are also facing tough financial times, will potentially supplement the aircraft market offer by selling out or reshaping their fleets. Moreover, the market is also sensitive to the intensifying production rates of the main aircraft manufacturers. Boeing and Airbus have increased production by 10% (compared to 2011) and are planning to deliver over 1110 new aircraft by the end of this year.

Uncertain prospects

Uncertain prospects

The diminishing price rates reflect the on-going financial uncertainty, particularly in the Western markets. Many carries are on the edge of bankruptcy and almost all of them are experiencing serious financial difficulties. As a result, the demand is shrinking, especially for the larger aircraft types. Moreover, any negative fluctuation in the airline community sends warning signals to other market players, forcing them to be more cautious with regard to any sizeable acquisitions.

Furthermore, the latest traffic growth analyses have shown that the North American market also shrank in the end of 2011and the first signs of its recovery were observed in end of winter only. Compared to other regions, the traffic growth rates in Europe were very modest, too. Naturally, the demand had to suffer and the aircraft prices had to go down.

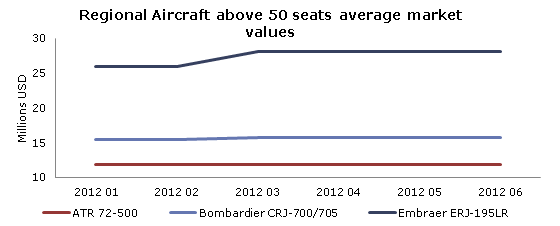

A chance for regional jets with 50+ seats

‘Unfortunately, some of the regions continue experiencing the aftermath of the recession, which naturally fetters carriers’ expansion plans. However, there are two sides to every coin. Driven to cut costs, some airlines are considering shifting to smaller, regional jets in order to optimize their route maps and lower operational costs,’ commented Gediminas Siaudvytis.

Table 2. Regional Aircraft above 50 seats average market values

The figures clearly indicate that the prices for regional jets with 50 plus seats, such as Embraer ERJ 195 and Bombardier CRJ 700, were in the green. These types of aircraft are becoming more and more popular while their manufacturers maintain stable production rates, which are quite moderate in comparison with those of the two major aircraft manufacturers. Moreover, while Airbus and Boeing are suffering from a high inter-competition (even between the models of the same manufacturer), the regional aircraft market is certainly not as intense. The market picture clearly indicates that the supply of some larger regional aircraft simply fails to keep up with the rising demand thus triggering the price growth even further.

‘The fact that more and more airlines prefer to operate the regional airplanes of 50 plus seats rather than long-haul narrow body models shows that carriers continue searching for ways to optimize their operations in the climate of economic uncertainty. This, along with the forecasts of drastically dropping carriers’ profits, clearly sends warning signals to the market that the industry, possibly, hasn’t recovered from the consecutive crises after all,’ commented the Deputy CEO of AviaAM Leasing.