Changing aircraft finance market – what are the possible alternatives to banks?

While aircraft manufacturers continue to increase their production rates in order to meet the global demand, the major changes can be observed in the aircraft financing segment. For some time now AviaAM Leasing experts have been observing a steady decline in the scope of the role played by banking institutions with regard to aircraft financing. Forced by various factors explained below, banks tend to increasingly minimise or sometimes even withdraw their presence on the market entirely. This naturally brings about additional challenges for airlines that are looking for a reputable institution, which would ensure the smooth financing of their future aircraft acquisitions and assist in other related transactions.

Increasing production rates

In the first half of 2012 Boeing delivered 237 aircraft, and another 334 are scheduled to reach their new owners by the end of the year. In the same period of time Airbus delivered 228 aircraft, and another 315 are scheduled for the remaining part of the year. The figures clearly indicate industry growth, since the total amount of the scheduled deliveries in 2012 is 10% higher than that in 2011. Moreover, manufacturers are planning to sustain similar growth rates in the upcoming years as well.

‘Aircraft manufacturers are enhancing their capabilities in order to shorten the delivery waiting list as much as possible. This naturally increases the demand for aircraft financing sources, since airlines need to pay for the ordered products. However, today finding funds for financing the acquisition of a new aircraft is becoming an increasingly challenging task for carriers, especially the smaller ones,’ commented the Deputy CEO of AviaAM Leasing Gediminas Siaudvytis.

Shrinking activity of banks

Shrinking activity of banks

The aftermath of the Global Economic Crisis has in many ways forced the existing financial institutions to reconsider all their current activities in order to ensure higher stability of their assets in the future. For instance, the Global and the European sovereign debt crises have triggered the implementation of the new regulatory requirements for the banking industry compelling some of the local banks to reduce their aircraft financing activities or even withdraw from the market altogether.

Moreover, despite the changes in the legislation, European banks themselves are becoming alarmingly de-motivated by the ongoing situation in the regional airline market, where several major carriers has gone bankrupt this year alone. Another unpleasant factor for those seeking aircraft financing solutions is the fact that some banks are finding it hard or are entirely unable to provide funds in US dollars, which is an undisputed primary currency in the aviation business. As a result, the price of borrowing is rising. The aftermath of the aforementioned: in 2011 the volume of bank-issued aircraft loans had dramatically fallen by 20%, according to Ascend.

Alternative sources of finance

In order to continue the implementation of their business strategies, airlines worldwide are forced to look for new ways to finance their aircraft acquisitions. Fortunately, other financial market players are quite enthusiastic about filling the market niche, which is being deserted by banks. For instance, various leasing companies along with sovereign wealth funds (SWF), institutional investors and private equity groups are increasingly stepping into the aviation finance market. Moreover, Western carriers, while reconsidering the finance strategies, are increasingly looking for solutions in Asia, as the local financial institutions are more likely to offer better terms of cooperation.

Table 1. Transactions in Europe Q2 2012 vs. Q1 2012

Leasing vs. ownershipThe situation in the aviation finance market eventually affects all market transactions, and even more so when it comes to the segment of older narrow–body aircraft. AviaAM Leasing experts point out that aircraft leasing is becoming a more popular financing solution with each year. Already today it may be stated that the volume of leasing transactions for a certain type of aircraft is definitely bypassing the volume of its sales transactions. Moreover, in Europe aircraft sales transactions in the Q2 of 2012 dropped by 12%, compared to the Q1 of 2012, while the lease transactions increased by 7%.

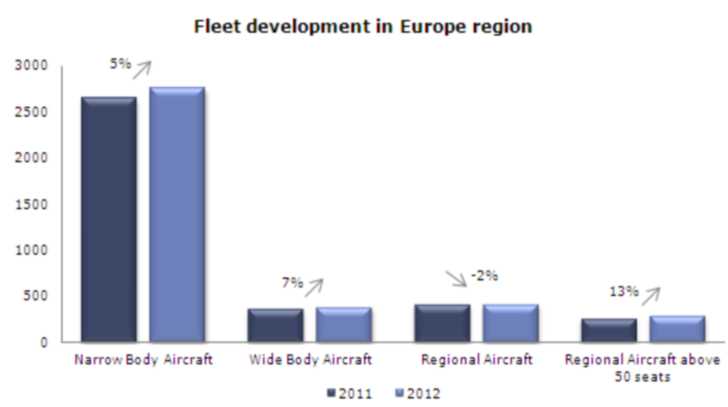

Table 2. Fleet development in Europe

Considering the sale/lease transactions issue more deeply, the majority of investors prefer to finance the acquisition of new aircraft only, while older aircraft are usually purchased under various leasing terms. During the previous year approx. 50% of all Airbus A320 aircraft sold were manufactured in 2011, 29% were built after 2000 and the remaining 21% were older than 14 years of age. At the same time, only 7% of all Airbus A320 leasing transactions in 2011 involved newly built aircraft, while 50% of the leased A320s were built after 2000 and 43% were older than 14 years of age. The situation is quite similar with regard to other aircraft types as well.

Table 3. Total sales transactions – Narrow-body aircraft

Table 4. Total lease transactions – Narrow-body aircraft

Market niche According to the industry figures, the number of aircraft transactions in the market is undoubtedly increasing along with the production rates of aircraft manufacturers. However, as the AviaAM Leasing experts have stressed, the aircraft financing market is rapidly changing. Today airlines are increasingly fond of the financial solutions that involve lease rather than traditional financing services offered by banks. What the industry offers is a great opportunity for the alternative financial market players, who could occupy the niche left by withdrawing bank financiers.