Historically the European air transportation market along with the North American market was considered being an exceptionally strong one. However, with the ongoing economic volatility in Europe local market players have been continuously facing with one of the weakest demand growth rates driving carriers for further optimization of their development plans. At the same time, backed up by the rising appetites of the aviation markets in Asia Pacific and the Middle East, commercial aircraft manufacturers continue to increase their production rates thus injecting the market with an even bigger amount of aircraft. These are the main factors which had contributed to an over 10% decline in average market prices for many mainline narrow body aircraft types throughout 2012.

Historically the European air transportation market along with the North American market was considered being an exceptionally strong one. However, with the ongoing economic volatility in Europe local market players have been continuously facing with one of the weakest demand growth rates driving carriers for further optimization of their development plans. At the same time, backed up by the rising appetites of the aviation markets in Asia Pacific and the Middle East, commercial aircraft manufacturers continue to increase their production rates thus injecting the market with an even bigger amount of aircraft. These are the main factors which had contributed to an over 10% decline in average market prices for many mainline narrow body aircraft types throughout 2012.

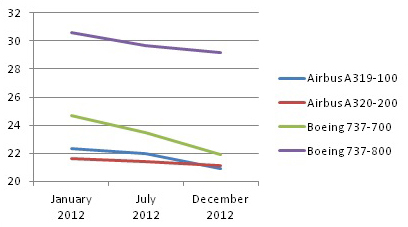

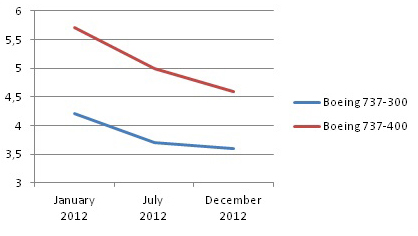

‘Whether it was Airbus A320 family or Boeing 737, the two work-horses of the global commercial aviation, the average market prices for these aircraft were falling during the entire 12-month period in 2012. The trend mainly affected the older generation aircraft. The average market prices for Boeing 737-300 and Boeing 737-400 declined by 14,3% and 19,3% respectively. The modern aircraft market which includes Airbus A320-200 and Boeing 737-800 has also seen no silver lining during 2012,’ commented Justinas Gilys, the Executive Director of AviaAM Leasing.

Table 1. Average market prices for mainline narrow body aircraft, millions USD.

Table 1. Average market prices for mainline narrow body aircraft, millions USD.

One of the factors which contributed to the downgrade of the prices is the ongoing financial uncertainty in the European and North American markets – once the strongest and main engines of air transportation industry’s development. According to the data provided by the IATA, the performance of European carriers in 2012 is expected to have been worth $400 million less than in 2011. The troubled European carriers, particularly from Southern Europe, along with some of their counterparts across the ocean have certainly triggered the negative trends on the global aircraft trade market.

Table 2. Average market prices for old generation narrow body aircraft, millions USD.

Table 2. Average market prices for old generation narrow body aircraft, millions USD.

‘Though some Western carriers experienced tough times or were even forced to leave the market in 2012, there is always Asia Pacific, the Middle East and other emerging aviation markets which keep the demand for aircraft deliveries sky high. Under the re-shaped route and fleet strategies (or bankruptcy) the troubled companies are phasing out the aircraft from their fleets, particularly the older ones, which were manufactured in late 1990s – early 2000s. However, many Asian carriers prefer to acquire either new aircraft, straight from the assembly line or those with little mileage on their dashboards,’ shares J. Gilys.

But not only the carriers which are restructuring their fleets and business model tend to fill the market with additional aircraft. Both Boeing and Airbus keep increasing their order and production rates. The European manufacturer delivered almost 590 aircraft in 2012, while securing 400+ new orders during the first three months of 2013 alone. At the same time, Boeing delivered over 600 commercial aircraft during the previous year and has received over 200 new orders since the beginning 2013.

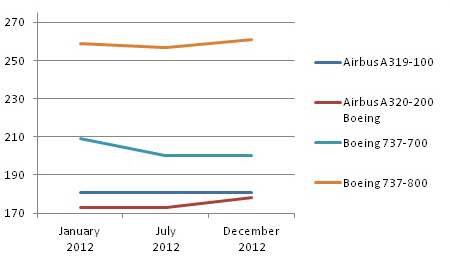

Table 3. Average lease rates for mainline narrow body aircraft, thousands USD.

Table 3. Average lease rates for mainline narrow body aircraft, thousands USD.

According to Mr. Gilys, while aircraft manufacturers are planning a further boost in their production rates some operators are keen to wait for an absolutely new generation, e.g. A320neo or B737max aircraft rather than invest into the currently produced older ones. ‘On the other hand, today many operators are avoiding long-term obligations. They prefer short and middle-term solutions which would allow them to be more flexible while entering new markets or adjusting to the volatile demand in the existing ones. That’s great news for aircraft leasing markets and the aforementioned trend has partially contributed to the relevant stability of lease rates throughout 2012,’ concluded the Executive Director of AviaAM Leasing.